Keep more of what you invest.

Get access to an advisor when you need it for an approximate 0.30% - 0.31% advisory fee in an all index portfolio.1

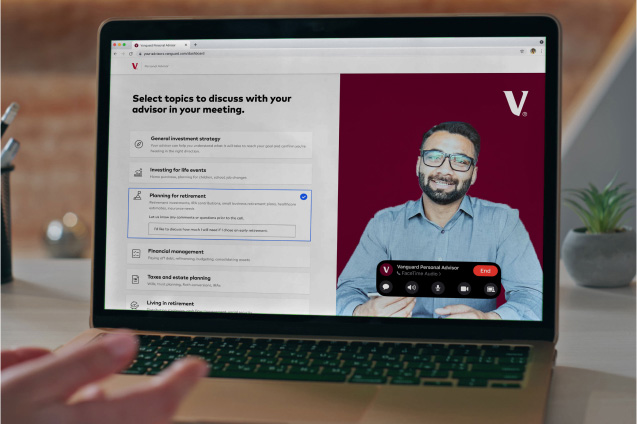

See how we tailor advice to you

$50,000

in minimum assets to enroll2

The 4 benefits of Vanguard Personal Advisor®

- Clarity

- Simplicity

- Confidence

- Support

Define and track your goals

Enjoy living with less mental math. Personal Advisor's advanced technology breaks down your investing goals and maps your progress for you, helping you see where your money stands at any point—from anywhere—on your laptop, tablet, or phone. And with access to an advisor, you can get the guidance you need to prioritize funding your goals.

Help reduce your investing stress

Why inflate your already packed to-do list? Instead, spend more time doing what you actually enjoy. With automated investment management built on Vanguard's DNA and a plan personalized to your goals, you can accomplish more while doing less.

Are you looking to combine your financial vision with your partner's or spouse's? Enroll as a couple to help improve tax efficiency and receive a shared strategy for your household.

Build your future on a solid foundation

Don't get caught up in the next investing fad. Vanguard's 4 investing principles are grounded in the long-term vision of giving you—and all investors—the best chance of success. With help from experienced advisors, strategies like tax-loss harvesting*, and a belief in staying the course, you can trust that Personal Advisor takes a holistic approach to building a healthy financial future.

Give your money a professional partner

Money is personal. Your financial advice should be too. With Personal Advisor, help is a phone call away. When life happens—including all things retirement—one of our advisors can help you navigate complex financial situations such as changes in income, adding a partner or spouse to your advised account, a birth or death in the family, and more.

Define and track your goals

Enjoy living with less mental math. Personal Advisor's advanced technology breaks down your investing goals and maps your progress for you, helping you see where your money stands at any point—from anywhere—on your laptop, tablet, or phone. And with access to an advisor, you can get the guidance you need to prioritize funding your goals.

Help reduce your investing stress

Why inflate your already packed to-do list? Instead, spend more time doing what you actually enjoy. With automated investment management built on Vanguard's DNA and a plan personalized to your goals, you can accomplish more while doing less.

Are you looking to combine your financial vision with your partner's or spouse's? Enroll as a couple to help improve tax efficiency and receive a shared strategy for your household.

Build your future on a solid foundation

Don't get caught up in the next investing fad. Vanguard's 4 investing principles are grounded in the long-term vision of giving you—and all investors—the best chance of success. With help from experienced advisors, strategies like tax-loss harvesting*, and a belief in staying the course, you can trust that Personal Advisor takes a holistic approach to building a healthy financial future.

Give your money a professional partner

Money is personal. Your financial advice should be too. With Personal Advisor, help is a phone call away. When life happens—including all things retirement—one of our advisors can help you navigate complex financial situations such as changes in income, adding a partner or spouse to your advised account, a birth or death in the family, and more.

Unique goals deserve personalized strategies

As an advice client, your financial journey drives the diversified blend of ETFs (exchange-traded funds) and mutual funds included in your portfolio—regardless of which investment option you choose.

Already have investments with us?

You may be able to keep some of your current investments when you enroll to lessen tax impacts.

Your personalized all-index investment option will center on low-cost Vanguard ETFs®, offering broad diversification covering nearly all aspects of U.S. and international stock and bond markets.

Who benefits from this investment option?

Investors looking for index funds that track broad U.S. and international stock and bond markets.

If you have higher taxable income, we'll use tax-exempt investments for your U.S. bond allocation in your taxable accounts.**

What are the advisory fees?

$35

You'll pay no more than $35 per $10,000 annually.2

What funds are used in this investment option?

Interested in this investment option?

Your personalized active/index investment option of Vanguard ETFs® and mutual funds will combine the chance for higher returns from actively managed funds with the broad diversification of index funds. It may also include up to 3 Advice Select funds available exclusively to our advice services clients.

Who benefits from this investment option?

Investors who are patient when active funds have periods of underperformance and are willing to pay a higher advisory fee with no guarantee of long-term outperformance.

If you have higher taxable income, we'll use tax-exempt investments for your U.S. bond allocation in your taxable accounts.**

What are the advisory fees?

$40

You'll pay no more than $40 per $10,000 annually.2

What funds are used in this investment option?

Interested in this investment option?

Your environmental, social, and governance (ESG) investment option will help to align with your preferences by substituting Vanguard ETFs® that apply prescreened ESG criteria defined by third-party index providers. It will also contain certain non-ESG bond ETFs to provide additional diversification.***

Why might you choose this investment option?

Investors who are seeking an investment option that helps to align their personal preferences. Though not as broadly diversified as total market funds, the ESG funds we use—when combined—include thousands of stocks and bonds to help balance investment risk and reward.

If you have higher taxable income, we'll use tax-exempt investments for your U.S. bond allocation in your taxable accounts.**

What are the advisory fees?

$35

You'll pay no more than $35 per $10,000 annually.2

What funds are used in this investment option?

Interested in this investment option?

Frequently asked questions

Enrollments in Personal Advisor require an aggregate $50,000 balance or greater in eligible Vanguard Brokerage Accounts.

For each taxable, traditional, Roth, or rollover IRA you wish to enroll, the entire balance must be in certain investment types (based on eligibility screening by Personal Advisor at the time of enrollment, see next question for more details) and/or the brokerage account's settlement fund.

To enroll, you'll need to meet the following requirements:

- You have a retail Vanguard Brokerage Account with a balance of at least $50,000. (If you're new to Vanguard, opening an account is simple.)

- You're a United States resident, or you have an APO/FPO/DPO mailing address.

- You’re at least 18 years of age. (At least age 19 in Alabama or Nebraska and at least age 21 in Mississippi.)

- You're not—or do not live in the same household as—a board member, executive, or someone who’s able to influence policy in a publicly traded corporation.

If you have a Vanguard-administered 401(k) retirement account, you may also be eligible to enroll.3 Restrictions may apply to certain organization members.

Vanguard Brokerage Option (VBO®) accounts offered by plan sponsors aren’t eligible for management by Personal Advisor. Special notice to non-U.S. investors.

Personal Advisor can manage eligible 401(k) retirement accounts and the following types of retail Vanguard Brokerage Accounts:

- Individual or joint tenants with rights of survivorship (JTWROS) taxable accounts.

- Traditional IRAs.

- Roth IRAs.

- Rollover IRAs.

- Inherited IRAs owned by natural, adult investors.

- Single-participant SEP-IRAs.

- Revocable trusts.

However, we recommend that you connect other Vanguard and non-Vanguard accounts as you plan your goals so we can incorporate them into your goal growth projections, and help you forecast your likelihood of meeting your long-term goals.

You'll incur expenses to invest in the underlying funds, collective investment trusts, and ETFs in your portfolio (i.e., expense ratios). If you're invested in ETFs, collective investment trusts, or mutual funds today, you're already paying these expenses. We credit the revenue received from your investment portfolio toward the gross advisory fee and deduct only the additional net advisory fee from your managed accounts.

In general, if you incur a fee that results in revenue for Vanguard or a Vanguard affiliate, it will be included in this credit amount. Certain regulatory required trading fees aren't considered revenue and are still incurred for trades within Vanguard Brokerage Accounts, but not credited. For more information about the fee structure, refer to Form CRS Conversation Starter questions and the Vanguard Personal Advisor Brochure.

Vanguard is one of the largest investment companies in the world with decades of experience and global recognition. Our highly respected investment managers, researchers, strategists, and economists have developed a deep expertise in all areas of investing. You'll get access to the best thinking of these Vanguard experts along with an investment strategy based on your personal goals that applies our methodologies to your situation. On top of that, our financial advisors are ready to help when you need it.

Personal Advisor might be a good fit for you if:

- You have questions about investing.

- You don't enjoy making investment decisions or you'd rather spend your time doing other things.

- It's tough to stick to a long-term plan or you often react to market volatility.

- You have to make complex financial decisions (Social Security, health care funding, or withdrawing retirement savings) and want help making these decisions.

- You believe in the power of diversification, low costs, and a long-term view.

- You want help managing your investments in a tax-efficient manner.

If you're looking for an advisor who will identify "hot" investment trends and actively trade to beat the market, Personal Advisor is NOT the right fit for you.

Personal Advisor offers a portfolio of actively managed mutual funds and index ETFs for Vanguard Brokerage Accounts. During the onboarding process, you'll take an assessment to determine whether you have the risk temperament for active strategies and can ride out periods of active underperformance. Incorporating active funds allows for greater portfolio personalization and the potential for better investment outcomes for those clients willing to pay a higher cost for that potential.

Focusing on investors' interests is what Vanguard was built on. We were founded on the mission to take a stand for investors to help give them the best possible chance for success. Learn more about our investment philosophy and company history.

We've always believed that successful investing can be simpler than many people think, but decades of experience have taught us that not everyone is as passionate about investing as we are—and that's okay.

For people who aren't as interested in creating and monitoring an in-depth financial plan (or delving into the nuances of asset allocation, rebalancing, taxes, and goal prioritization), we're here to help. We also believe that talking to an advisor can be helpful if things get a bit stormy, whether it's in the market or your personal life.

If you don’t already have an account with Vanguard, you’ll be asked to create one with a username and password. Then you'll fill us in on information related to your financial profile.

- Expect to answer questions related to your risk tolerance, short- and long-term financial goals, and general financial health. This helps us create a customized portfolio just for you.

- You may schedule an appointment with an advisor before enrolling to ensure our advice offer and portfolio construction plan suits your personalized needs.

- After enrolling, you'll have access to an advisor at any time. Simply schedule an appointment on your Personal Advisor dashboard.

- Additionally, you'll continue to receive nudges to complete your financial picture even after enrolling. This may include setting up automated contributions to meet your goals, defining your emergency savings, choosing a Medicare plan prior to becoming eligible, preparing for healthcare costs in retirement, and more.

1Enrollments in Personal Advisor require an aggregate $50,000 balance or greater in eligible Vanguard Brokerage Accounts. For each taxable, traditional, Roth, rollover, or inherited IRA you wish to enroll, the entire balance must be in certain investment types (based on eligibility screening by Personal Advisor at the time of enrollment) and/or the brokerage account's settlement fund.

2Vanguard Personal Advisor charges Vanguard Brokerage Accounts an annual gross advisory fee of 0.35% for its all-index investment options and 0.40% for an active/index mix. These services reduce those fees by the amount of revenue that Vanguard (or a Vanguard affiliate) retains from your portfolio in order to calculate your net advisory fee. Note that this fee doesn't include investment expense ratios. Please review the service’s advisory brochure for more fee information.

You should consult your plan fee disclosure notice for the applicable annual gross advisory fees that apply to your 401(k) account.

3Vanguard-administered 401(k) retirement accounts are only eligible for management by Personal Advisor if the plan sponsor has elected to offer Personal Advisor to the plan's participants and the participants meet the eligibility criteria.

All investing is subject to risk, including the possible loss of the money you invest. Diversification does not ensure a profit or protect against a loss.

Visit vanguard.com to obtain a Vanguard mutual fund or Vanguard ETF prospectus or, if available, a summary prospectus, which contains investment objectives, risks, charges, expenses, and other information; read and consider it carefully before investing.

All costs associated with fund expense ratios still apply at all times.

*Tax-loss harvesting involves certain risks, including, among others, the risk that the new investment could have higher costs than the original investment and could introduce portfolio tracking error into your accounts. There may also be unintended tax implications. We recommend that you carefully review the terms of the consent and consult a tax advisor before taking action.

**Municipal bond fund distributions, including any market discount recognized by the Fund's investments, may be taxable as ordinary income or capital gains. A majority of the income dividends that you receive from the Fund are expected to be exempt from federal income taxes. However, a portion of the Fund’s distributions may be subject to federal, state, or local income taxes or the federal alternative minimum tax. You should consult your own tax advisor with respect to any particular U.S. or non-U.S. tax consequences of your investment in the Fund.

***To maintain diversification, this portfolio option will also include non-ESG investments to achieve your target asset allocation for international and domestic bonds.

The ESG investment option gives Personal Advisor clients the ability to substitute certain existing holdings with Vanguard ETFs that invest according to an index that has been pre-screened based on ESG factors determined by a third-party index provider. There is no guarantee that the ESG investment option will perform better than the other investment options.

ESG funds are subject to ESG investment risk, which is the chance that the stocks or bonds screened by the index provider for ESG criteria generally will underperform the market as a whole or, in the aggregate, will trail returns of other funds screened for ESG criteria. The index provider's assessment of a company, based on the company's level of involvement in a particular industry or the index provider's own ESG criteria, may differ from that of other funds or of the advisor's or an investor's assessment of such company. As a result, the companies deemed eligible by the index provider may not reflect the beliefs and values of any particular investor and may not exhibit positive or favorable ESG characteristics. The evaluation of companies for ESG screening or integration is dependent on the timely and accurate reporting of ESG data by the companies. Successful application of the screens will depend on the index provider's proper identification and analysis of ESG data.

Vanguard’s advice services are provided by Vanguard Advisers, Inc. (“VAI”), a registered investment advisor, or by Vanguard National Trust Company (“VNTC”), a federally chartered, limited-purpose trust company.

The services provided to clients will vary based upon the service selected, including management, fees, eligibility, and access to an advisor. Find VAI’s Form CRS and each program’s advisory brochure here for an overview.

VAI and VNTC are subsidiaries of The Vanguard Group, Inc., and affiliates of Vanguard Marketing Corporation. Neither VAI, VNTC, nor its affiliates guarantee profits or protection from losses.

If you decide to manage your investments on your own, you can buy and sell Vanguard ETF Shares through Vanguard Brokerage Services® or another broker (which may charge commissions). See the Vanguard Brokerage Services commission and fee schedules for full details. Vanguard ETF Shares are not redeemable directly with the issuing fund other than in very large aggregations worth millions of dollars. ETFs are subject to market volatility. When buying or selling an ETF, you will pay or receive the current market price, which may be more or less than net asset value.

All investing is subject to risk, including the possible loss of the money you invest. Diversification does not ensure a profit or protect against a loss.

Visit vanguard.com to obtain a Vanguard mutual fund or Vanguard ETF prospectus or, if available, a summary prospectus, which contains investment objectives, risks, charges, expenses, and other information; read and consider it carefully before investing.

All costs associated with fund expense ratios still apply at all times.

1Vanguard Personal Advisor charges Vanguard Brokerage Accounts an annual gross advisory fee of 0.35% for its all-index investment options and 0.40% for an active/index mix. These services reduce those fees by the amount of revenue that Vanguard (or a Vanguard affiliate) retains from your portfolio in order to calculate your net advisory fee. Note that this fee doesn't include investment expense ratios. Please review the service’s advisory brochure for more fee information.

2Enrollments in Personal Advisor require an aggregate $50,000 balance or greater in eligible Vanguard Brokerage Accounts. For each taxable, traditional, Roth, rollover, or inherited IRA you wish to enroll, the entire balance must be in certain investment types (based on eligibility screening by Personal Advisor at the time of enrollment) and/or the brokerage account's settlement fund.

*Tax-loss harvesting involves certain risks, including, among others, the risk that the new investment could have higher costs than the original investment and could introduce portfolio tracking error into your accounts. There may also be unintended tax implications. We recommend that you carefully review the terms of the consent and consult a tax advisor before taking action.

**Although the income from a municipal bond fund is exempt from federal tax, you may owe taxes on any capital gains realized through the fund's trading or through your own redemption of shares. For some investors, a portion of the fund's income may be subject to state and local taxes, as well as to the federal Alternative Minimum Tax.

***To maintain diversification, this portfolio option will also include non-ESG investments to achieve your target asset allocation for international and domestic bonds.

The ESG investment option gives Personal Advisor clients the ability to substitute certain existing holdings with Vanguard ETFs that invest according to an index that has been pre-screened based on ESG factors determined by a third-party index provider. There is no guarantee that the ESG investment option will perform better than the other investment options.

ESG funds are subject to ESG investment risk, which is the chance that the stocks or bonds screened by the index provider for ESG criteria generally will underperform the market as a whole or, in the aggregate, will trail returns of other funds screened for ESG criteria. The index provider's assessment of a company, based on the company's level of involvement in a particular industry or the index provider's own ESG criteria, may differ from that of other funds or of the advisor's or an investor's assessment of such company. As a result, the companies deemed eligible by the index provider may not reflect the beliefs and values of any particular investor and may not exhibit positive or favorable ESG characteristics. The evaluation of companies for ESG screening or integration is dependent on the timely and accurate reporting of ESG data by the companies. Successful application of the screens will depend on the index provider's proper identification and analysis of ESG data.

3Based on enrolling accounts holding assets in the settlement fund that are invested in a portfolio of Vanguard Total Stock Market ETF, Total International Stock ETF, Total Bond Market ETF, and Total International Bond ETF.

You should consult your plan fee disclosure notice for the applicable annual gross advisory fees that apply to your 401(k) account.

4Vanguard-administered 401(k) retirement accounts are only eligible for management by Personal Advisor if the plan sponsor has elected to offer Personal Advisor to the plan's participants and the participants meet the eligibility criteria.

Vanguard’s advice services are provided by Vanguard Advisers, Inc. (“VAI”), a registered investment advisor, or by Vanguard National Trust Company (“VNTC”), a federally chartered, limited-purpose trust company.

The services provided to clients will vary based upon the service selected, including management, fees, eligibility, and access to an advisor. Find VAI’s Form CRS and each program’s advisory brochure here for an overview.

VAI and VNTC are subsidiaries of The Vanguard Group, Inc., and affiliates of Vanguard Marketing Corporation. Neither VAI, VNTC, nor its affiliates guarantee profits or protection from losses.

If you decide to manage your investments on your own, you can buy and sell Vanguard ETF Shares through Vanguard Brokerage Services® or another broker (which may charge commissions). See the Vanguard Brokerage Services commission and fee schedules for full details. Vanguard ETF Shares are not redeemable directly with the issuing fund other than in very large aggregations worth millions of dollars. ETFs are subject to market volatility. When buying or selling an ETF, you will pay or receive the current market price, which may be more or less than net asset value.