Vanguard research shows a trend toward investors contributing earlier to their IRAs.

3 ways to maximize your IRA contributions

Did you know you can contribute to your IRA up to 15 months before the tax-filing deadline? Vanguard research shows that more investors are taking advantage of early contributions, but there are still quite a few who potentially pay the price for procrastinating.

As you work to complete your 2025 taxes, it’s the perfect time to get a jumpstart on 2026 contributions—contribute to your IRA now instead of waiting until next year. Here are some tips gathered from insights into Vanguard investors’ contribution behavior over the past several years that show why this is a good practice:

1. Contribute early to take advantage of compounding.

Although we’ve seen an increased trend of “early-bird” contributors (shown in the first graph below), there’s still a significant percentage of investors who wait until the next year to contribute. Many even hold off until April. Waiting can result in potentially paying a steep procrastination penalty by missing out on the power of compounding. As you can see in the second graph, that simple contribution timing decision can make a significant difference!

Investors shift timing of IRA contributions

Note: From 2019 to 2022, contribution rates in January nearly doubled, and contributions in April of the next year dropped by about one-third.

Source: Vanguard.

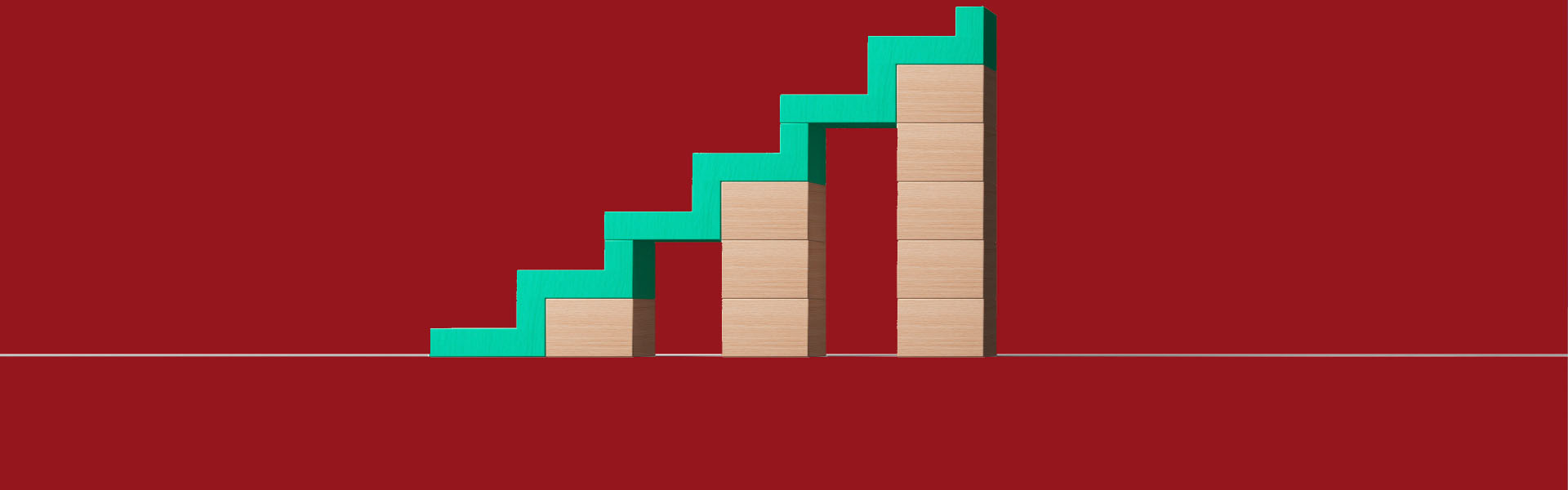

Early contributors get the compounding

This example is based on an investor making a one-time, lump-sum contribution of $7,500 in January of the current year (early) and realizing a 6% return versus a one-time, lump-sum contribution of $7,500 in April the following year (late) realizing a 6% return. In each example, you're contributing a total of $225,000 to your IRA over the course of 30 years. The difference in earnings is due entirely to the timing of your contributions.

Note: This hypothetical example doesn’t represent the return on any particular investment and the rate isn’t guaranteed.

Source: Vanguard.

2. Set up recurring contributions to benefit from tax-advantaged growth.

If you’re not able to contribute a lump sum early in the year, you can still participate in the tax-advantaged growth by contributing during the year through a recurring contribution program. For example, if you want to get to that $7,500 maximum for the 2026 tax year, consider establishing a $625 monthly contribution.

3. Avoid decoupling contribution and investment decisions so contributions aren’t parked in cash.

Some investors seem to be focused on the act of getting their contribution in rather than making sure it’s invested; like it’s a check-the-box exercise. By decoupling the contribution and investment decisions they can end up leaving money sitting in cash for months before they invest it, thereby missing out on the potential returns that could have been generated. To avoid paying the potential opportunity cost of being uninvested, make sure to take that extra step when you contribute and consider investing right away in either a target date fund or balanced fund.

Get a jumpstart on next year

So, as you’re wrapping up your 2025 tax returns, which are due on April 15, 2026, take some time to get ahead of next year by making and investing your IRA contribution now.