Learn how a break-even tax rate approach may help evaluate traditional to Roth IRA conversions and support more informed retirement tax planning decisions.

A "BETR" calculation for the Traditional-to-Roth IRA conversion equation

The Roth IRA offers tax-free investment growth and tax-free withdrawals during retirement. For many investors, these features make the Roth come out ahead in the ongoing traditional-versus-Roth IRA debate. Even so—and thanks mainly to a combination of legacy assets and the larger sums rolled over from employer-sponsored retirement accounts—the lion’s share of all IRA assets are held within traditional accounts.1

“Despite the advantages of conversion, there isn’t always a clear-cut path when deciding whether to convert a traditional to a Roth IRA,” says Vanguard’s Joel Dickson, global head of advice methodology. “The traditional wisdom says to convert if you expect your tax rate to rise in retirement. And yet, a Roth conversion can be favorable for far more investors than this rule of thumb would suggest.”

Dickson and Vanguard wealth planning specialist Boris Wong champion the break-even tax rate (BETR) as a superior method for calculating the point at which a Roth conversion makes sense.

What is the break-even tax rate (BETR)?

With the BETR approach, future tax rate expectations are but one factor in the conversion decision. The approach levels up the analysis by taking into account crucial factors like conversion-tax proceeds paid from account assets held outside the IRA, the tax basis of the IRA account, and future plans to contribute to the IRA (typically using a backdoor strategy).

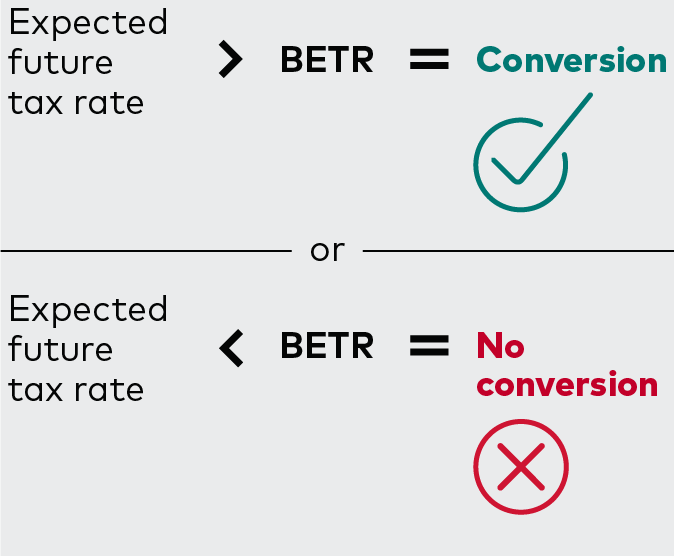

At its most basic form, BETR is that future tax rate at which the after-tax withdrawal value for an investor would be the same in both the no-conversion and conversion scenarios.

In a sense, the conversion decision will depend on this single figure. If an investor’s future tax rate is greater than the BETR, it makes sense to convert; if the future tax rate is lower than the BETR, it doesn’t.

How to use the single-figure break-even tax rate to decide if a Roth conversion is the best choice

How to use the single-figure break-even tax rate to decide if a Roth conversion is the best choice

How to lower the BETR

Even better: The BETR is not a static number. There are investor choices that can lower the rate, and this, in effect, expands the pool of those who could ultimately benefit from the long-term tax advantages of a Roth conversion. Investors can:

- Pay conversion taxes from a taxable account. Tapping into a separate cache of cash allows the full value of the IRA to move to a tax-advantaged account. The more tax-inefficient the account used to pay the conversion tax, the lower the BETR (and the greater the benefit of converting).

- Invest over a longer time horizon. The longer the time frame, the greater the potential for Roth assets to compound tax-free, and the lower the BETR for Roth-converting investors who pay the conversion tax from taxable assets.

- Use the Roth conversion as an opportunity to make future backdoor Roth IRA contributions. Only investors filing under a certain income limit qualify for Roth IRA contributions—but the two-step backdoor Roth conversion strategy is open to investors at all income levels. By using the backdoor method, you can contribute up to $7,500 ($8,600 if you’re 50 or older) to your Roth IRA for the 2026 tax year. Over time, that adds up to a lot of tax-advantaged investment opportunities. And don’t forget to consider your IRA’s tax basis. Nondeductible contributions will not be taxed again during a Roth conversion. This, too, will lower the BETR.

Other often-overlooked considerations

“The value of a Roth conversion is often underestimated and underappreciated,” says Wong. That’s because the tax benefits of a Roth account are difficult to capture fully with the traditional rule of thumb—or even when with the more sophisticated BETR calculation. Those benefits include:

- Greater potential for tax advantages after the loss of a spouse. As of 2026, a couple with a $60,000 annual income falls in the 12% tax bracket, while a widowed single filer with the same income may land in the 22% bracket.

- Reduced required minimum distribution (RMD) demands. Roth IRAs have no RMD, and they are not subject to RMD rules during the owner’s lifetime.

- Enhanced flexibility around the Medicare and Social Security tax cliffs. Roth IRA withdrawals do not affect the taxable income levels that affect these benefits.

“Paying taxes now to avoid higher taxes in the future can be a valuable strategy for many investors,” Dickson says. “The BETR calculation can make a traditional-to-Roth conversion more accessible than the conventional analysis suggests.”