Learn how to avoid costly mistakes when paying for emergencies. Vanguard offers tips on managing your emergency fund and protecting your finances.

Avoid these 5 ways to pay for emergencies

1. Using credit cards

Emergencies are never fun to begin with—do you really want to make it worse by paying more than you have to? Interest rates on credit cards can be sky-high. And don't forget about potential late fees, the risk of going over your credit limit, and the fact that your credit score could take a hit if you don't make your payments on time.

2. Withdrawing your retirement money

Using money that you've earmarked for retirement (or another goal, like college) could hurt you in a number of ways.

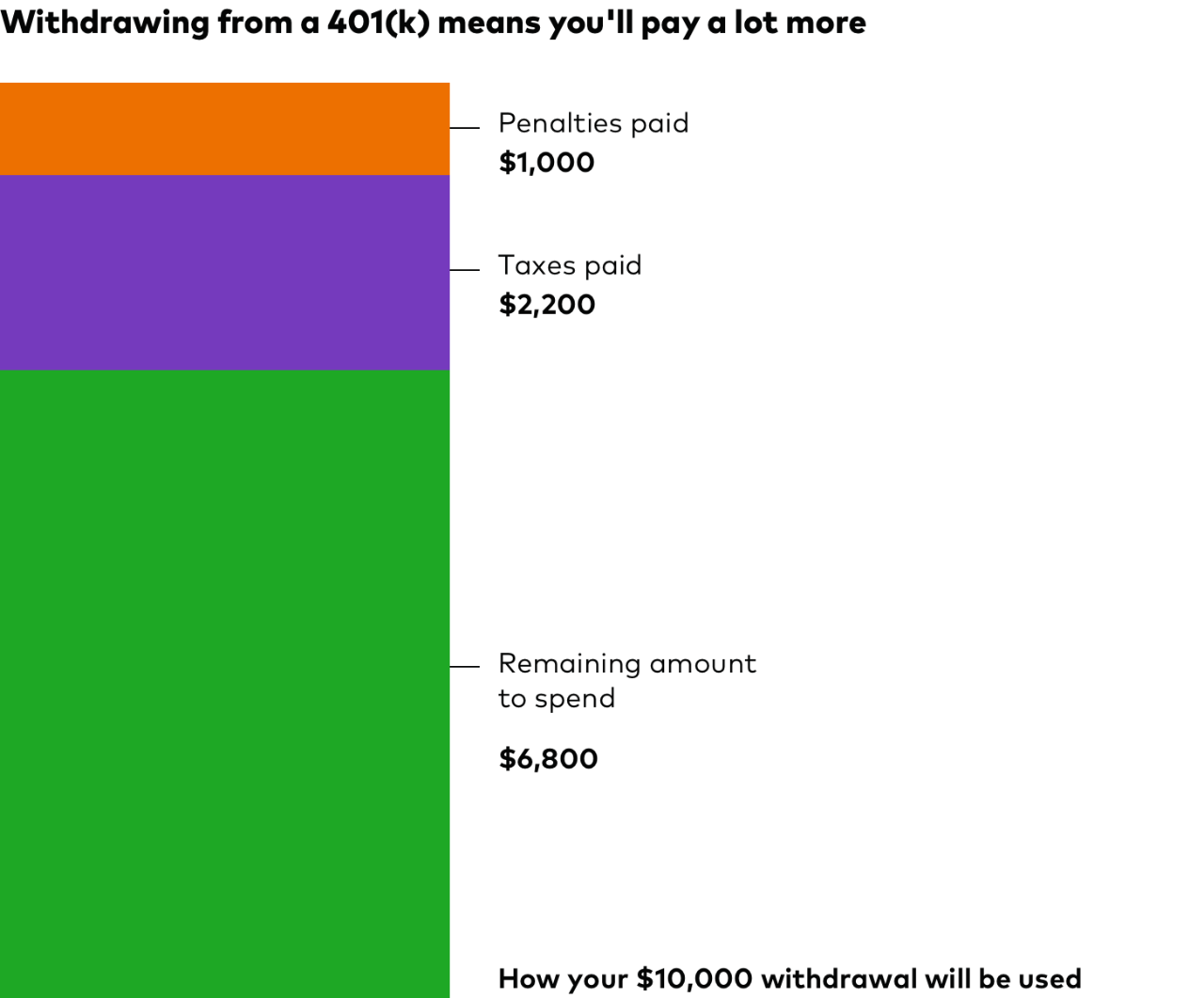

If you take money from a tax-deferred account—a traditional IRA, a 401(k), or a 529, for example—you could be hit with an early withdrawal penalty and have to pay income taxes.*

So, for example, if you withdraw $10,000, you could be looking at total taxes and penalties of $3,200 (if you're in the 22% tax bracket)—leaving you with $6,800 to deal with your emergency.

And that might not even be the worst part.

The money you withdraw could eventually threaten your ability to reach your goal. Going back to our example, $10,000 might seem like a small drop in your retirement bucket, but you'll also miss out on years of compounding. That means your balance could be up to $57,000 less than if you hadn't made the withdrawal.

The true cost of taking a retirement withdrawal

This hypothetical example assumes that you miss out on 30 years of compounding at an annual 6% return. It doesn't represent any particular investment nor does it account for inflation and the rate is not guaranteed.

What about taking a loan from your 401(k) instead? Remember that if you fail to pay back the loan—or if you leave your employer and can't repay the loan immediately—you'll face the same taxes and penalties that come with a withdrawal.

3. Counting on family or friends

Sure, someone might be willing to lend you money in a time of need … at least the first time. But wouldn't you feel better not placing a financial burden on those you care about?

4. Relying on insurance

You pay for insurance so that when an emergency crops up, you're all set, right? In reality, sometimes insurance claims are denied, require you to pay a deductible, or are only partially covered.

Trying to insure your way out of all possible financial hardships isn't a great idea, either.

Instead, think about taking any money you spend to insure electronics, appliances, and pet care and putting it in your emergency fund.

If you truly need the money, you'll be covered. If you don't, congratulations—your emergency fund just got a little fatter.

5. Selling risky investments

Maybe you've got some "fun money" stashed away in stock or bond investments, but you shouldn't consider that an emergency fund.

By definition, emergencies happen when you're not expecting them. If you need to pay for them by tapping into your stock or bond holdings at a time when they're taking a beating in the market, you'll lock in your losses.

DID YOU KNOW?

47% of people in the United States don't have a rainy day fund that would cover 3 months of expenses.

Source: FINRA Investor Education Foundation National Financial Capability Study, 2022.

So how should you pay for emergencies?

Opening a savings fund to use strictly for unexpected expenses has its benefits.